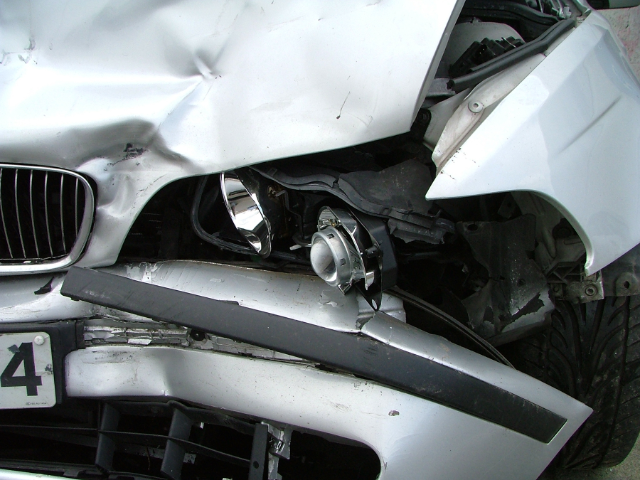

With the escalating price of motor vehicles, not only in South Africa but around the world, motor insurance is more important than ever. The ever-increasing number of vehicles on our roads leads to greater congestion and less room for everyone. This means that your chances of having an accident increase every year. As motor vehicles are probably the most expensive thing that you will buy in your lifetime, it's worth ensuring that it is insured should anything happen to it.

Related: Tips to get the best car insurance price

Insure exists to help ensure that you're left in the same financial position before an incident, as you are after it; be it theft, fire or accident. It's for this reason that a tailored, comprehensive insurance policy is crucial when buying a car, either new or used. It may seem like an unnecessary expense every month and can feel like burning money, but the dividends pay off sooner or later.

What is an excess?

The best way to think of an excess is to think of it as a self-insurance portion of your insurance. It's an amount that you pay-in when claiming to reach the required payout total. By contributing to this pay-out on your own, the insurer doesn't have to cover the entire amount and this lowers your monthly premiums. While this is one of the benefits of an excess, one must be careful not to use it as the sole means of reducing your premiums, especially if you are unable to afford the excess amount at the time of claiming.

Bumping your excess up also counteracts the benefit of having insurance for small claims. A small bump could cost say R3 000 to repair but with a R5 000 excess, it would be counterintuitive to claim as you would have to pay the minimum amount of R5 000 for that R3 000 repair.

It's wise to set aside the excess amount in a savings account where it can accrue interest and where it isn't touched so that it is readily accessible when you need to claim.