Car financing is a specialised field , with many terms and phrases that are gobbledegook to the average person. Here is a quick guide to what some of those terms mean.

Deposit

This is the amount you will need to save up, before you set out to borrow the rest of the money needed for a new or second-hand car. It is possible to get a 100 % loan on a car, but finance houses will usually require a deposit ranging from 10 or 20 % of the purchase price. So, if the car costs R200 000, a 10% deposit will amount to R20 000.

Interest

The banks or finance houses (FSPs) will charge you interest on the money they loan you. This interest will be paid off as part of your monthly repayment, while a part of each payment will also go to re-paying the original amount that you borrowed. You can generally get a loan at a fixed interest rate, where the interest you pay will be an agreed amount for the duration of the loan period, or one that varies according to something called the Prime Interest Rate.

Related: Check out our car finance calculator to see how much your repayments would be.

Prime Rate

The Prime Lending Rate – normally referred to by finances houses merely as “Prime” – is determined by the South African Reserve Bank. This rate fluctuates, and has been set at 7.25 % since end-2020. Depending on your credit record and provable income, an FSP may typically lend you money on a car repayment scheme, at an interest rate of between 7.5 % and 10.5 %. In other words, between “Prime” and “Prime-plus three”.

Paying a reasonable deposit on a car, and submitting proof that you are more than capable of meeting those monthly repayments on your budget, will usually encourage a finance house to offer you a competitive interest rate on your repayment contract. Not all offers are equal, though, so shop around for the best finance deal for your pocket.

Instalment Finance (Hire Purchase)

This is the most straight forward type of car financing. Repayment period options for instalment financing typically range from 12 months to 72 months, or one to six years. The shorter the loan period, the higher your monthly repayments will be. But the longer the instalment period, the more interest you will be paying on the amount you borrowed.

Balloon Payment

This a repayment scheme that allows you to effectively repay a lump sum of money on the loan at the end of the repayment contract, rather than paying a deposit up front. Unfortunately, it also means that you'll be owing a substantial amount on your car, even after making years of payments. This amount will then either have to be recovered (settled with the FSP) by selling the vehicle (hopefully for more than the settlement amount), or re-financing the outstanding amount.

The benefit of a balloon payment is that it allows you buy a car before you have saved up a deposit, and still enjoy driving the car immediately. Your monthly payment on a balloon scheme will be lower than if you had simply opted for a straight instalment finance scheme, but there's a catch...

Balloon Payment Pitfalls

Many reputable finance houses recommend avoiding the balloon payment scheme. For example, with a 20 % balloon payment coming due at the end of a 72 month contract for a R 200 000 car loan, this will mean that after paying your last (more affordable) monthly instalment, you will be due for lump sum of R40 000.

In many cases, the only way of raising that amount of money is to sell the car. And cars depreciate considerably in value each year, especially if they are not properly maintained. You may find that your car’s market value at the end of the finance contract may barely cover the cost of that balloon payment. Which means you will be back where you started, after six years and scrimping and scraping to make all those monthly repayments!

Related: Get a comprehensive run-down on all matters pertaining to car finance here.

Settlement

This the term referred to by finance houses, for paying off your loan agreement earlier than the agreed repayment period. This typically happens when you want to buy a new (or newer or different) car before the end of the agreed loan period.

The finance house will then work out a settlement amount. This won’t normally happen before a 12-month period has gone by since you bought the car, as finance companies make their money from the loan's interest, and the longer the loan period, the more money they make. Read that contract carefully, regarding this clause!

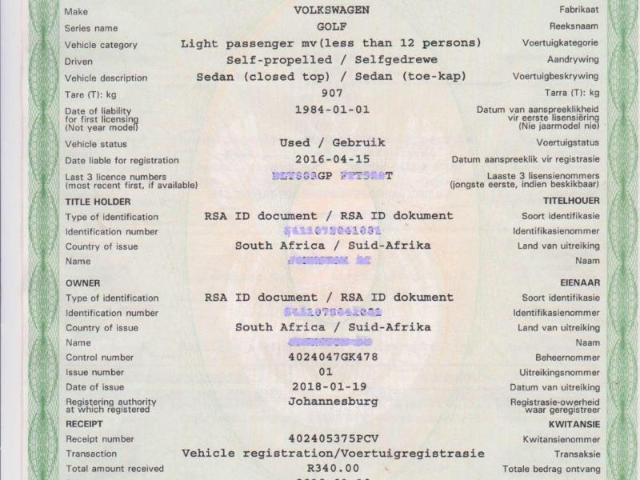

Title Holder

This is very important! When you enter into a car financing contract, the car will be registered in your name as the “owner”. But, until you have made the last payment on the loan, the finance house will be listed on the registration document as the “title holder": The finance house will retain the registration document until that final payment. In a real sense, the finance house owns the car until you have made that final payment!

Once the car is paid off, the owner should then approach the finance house for the release of the registration certificate, as well as a document stating that the car has been paid for in full. The owner should then take these documents to the nearest (NATIS) traffic authority and have the car’s registration updated, so that the owner is now also the title holder. You cannot legally sell a car unless you are listed as both the owner and the title holder!

Guaranteed Future Value (GFV)

According to Ghana Msibi, currently Wesbank’s CEO in their motor division, the temptation of a new car can sometimes lure a buyer into a commitment that isn’t an ideal fit for their budget.

“Fortunately, there are flexible finance options for buyers to choose from, “ says Msibi. “WesBank wants to ensure that all consumers fully understand what’s available, so they can make smarter, more responsible decisions on their car-buying journey.”

One of these options that Msibi highlights is the GFV option.

“Guaranteed Future Value, also known as GFV or any number of brand-specific titles, is becoming an increasingly popular form of vehicle finance in South Africa. It is important to note that a vehicle’s value begins depreciating (losing monetary value) from the moment it leaves the showroom floor. In line with this depreciation, a GFV plan calculates what the future monetary value of a vehicle will be if specific conditions of vehicle condition, mileage and maintenance are met. This future value is guaranteed at the start of the agreement."

“This makes planning ahead easier, as consumers know exactly what their car will be worth once the pre-determined contract term (usually between three and four years) is reached. The customer is given three choices at this point – they can either enter into another GFV deal and drive away in new vehicle, settle the outstanding amount and own the vehicle, or simply return the vehicle to the respective dealership and walk away (provided the driver didn’t exceed the allotted mileage and the vehicle is in acceptable condition).

“With a GFV plan, a consumer is essentially only paying for the use of the car. This is why it’s important to know more or less the distance the vehicle will cover during the GFV term. Consumers are liable for penalties if any conditions of the GFV agreement aren’t met.”